BOOKKEEPING - WHAT SMALL BUSINESSES HAVE IN COMMON

What Bookkeeping and Accounts is my Canadian Company Obligated to do?

All companies in Canada must respect the International Financial Reporting Standards (IFRS) and the generally accepted accounting principles (GAAP) when filing accounting documents. And the Canada Revenue Agency (CRA) states that "if you file your return on time, keep your records for a minimum of six years after the end of the taxation year to which they relate." However, the six years is from the end of the period for which the tax return was filed. So, as an example, for a tax return filed in 2020, you must keep the records until December 31 of 2026 (one day less than seven years). We would simply recommend keeping company accounting records for seven years to avoid confusion.

To keep bookkeeping records in a logical, comprehensible and compliant way – to make it easy to understand if the CRA do decide to audit, they should ideally be set up in a standardized manner. The following outlines the commonalities of bookkeeping systems for Canadian companies across different types of businesses – though if this seems complicated, or your company has some specific accounting requirements, it may be best to engage the services of a local and well rated bookkeeping service. If you do decide to set it up yourself, these are the basics of setting up a bookkeeping system in a standardized way.

Chart of Accounts

The starting point of any accounting system is to set up a chart of accounts. A chart of accounts is the listing of all the account names and numbers contained in the general ledger. Each account in the chart of accounts records information for a particular type of transaction. For example, separate accounts would almost always be required for each bank account, together with one expense account to record bank service charges and separate accounts for each bank loan. Together all the accounts related to the company make up the chart of accounts.

The starting point of any accounting system is to set up a chart of accounts. A chart of accounts is the listing of all the account names and numbers contained in the general ledger. Each account in the chart of accounts records information for a particular type of transaction. For example, separate accounts would almost always be required for each bank account, together with one expense account to record bank service charges and separate accounts for each bank loan. Together all the accounts related to the company make up the chart of accounts.

The accounts are organized into logical categories. The categories are used to calculate and update the total values of the assets, liabilities, equity, revenues, and expenses as transactions are posted. When using a computerized accounting system, these calculations and updates are done automatically.

The chart of accounts is most useful if it is specific to the industry. Many computerized accounting systems come with pre-configured account classifications that can be applied to particular businesses.

Often accounts will need to be changed, renumbered or renamed to suit the specific business. Others can be removed if not being used and some new accounts may have to be added.

In a computerized accounting system, new accounts may be added at any time and account names may be changed at any time. However, there are generally restrictions on deleting accounts in a computerized accounting system. The greatest variation in account numbers usually occurs in the income statement accounts.

Designing the Chart of Accounts

To set up a customized chart of accounts, the names and numbers of the existing accounts will need to be modified/deleted or new ones added. When numbering new accounts, the numbers assigned must fall into the ranges that are already established in the template being used.

For example, in a basic accounting software program accounts added must respect the numbering scheme, generally based on four-digit account numbers.

- Assets 1000 to 1999

- Liabilities 2000 to 2999

- Equity 3000 to 3999

- Revenues 4000 to 4999

- Expenses 5000 to 5999

In other programs, such as a premium edition, an extended numbering system may be set up. The range of the account numbering can be expanded, and digits can be added or removed or the start and end numbers used by any of the account groups or classes can be changed.

An expanded numbering system must follow the established account numbering order. It is possible, however, to leave gaps in the numbering system for later use.

An example of an extended numbering system:

Some programs allow departmental accounting. Departments represent sections of the company that may need to be examined individually.

These sections can be the business units of the company (such as Marketing, Accounting, Warehouse, Human Resources or Office Administration). Departments may be used for separate locations (such as Winnipeg, Calgary, Toronto, and St. John’s)

An example of how a chart of accounts might look if Departmental Accounting is to be used:

The list of departments:

1000 Marketing

2000 Accounting

3000 Warehouse

4000 Human Resources

5000 Office Administration

The supplies accounts in the chart of accounts by department would be:

5400 – 1000 Supplies Marketing

5400 – 2000 Supplies Accounting

5400 – 3000 Supplies Warehouse

5400 – 4000 Supplies Human Resources

5400 – 5000 Supplies Office Administration

These additional accounts are not required in an accounting software program that allows departments to be set up. Only one account “5400 – Supplies” would be set up, and the expense allocated to the department.

Setting up the chart of accounts to permit departmental accounting allows reports to be printed, for example, for each supply account by department and also a total of all supplies. Similarly, financial statements could be printed for each department or group of departments or for the total of the departments.

Classifying Liabilities

A current liability is a short-term obligation, as at the balance sheet date, which is expected to be paid out of the current assets listed on the same balance sheet. A current liability is expected to be paid during the coming year or the normal operating cycle of the business, whichever is longer. Examples of current liabilities include accounts payable, wages payable, short term notes payable, income taxes payable, and any other obligations that have been incurred but have not yet been paid and which are to be settled in the short term.

A current liability is a short-term obligation, as at the balance sheet date, which is expected to be paid out of the current assets listed on the same balance sheet. A current liability is expected to be paid during the coming year or the normal operating cycle of the business, whichever is longer. Examples of current liabilities include accounts payable, wages payable, short term notes payable, income taxes payable, and any other obligations that have been incurred but have not yet been paid and which are to be settled in the short term.

A long-term liability is any obligation of the enterprise that is not a current liability. They have maturities that extend beyond one year from the balance sheet date (or one operating cycle if longer than a year). Examples of long-term liabilities include term bank loans, mortgages and bond payable.

Long-term liabilities should be reclassified as current liabilities if they become due within one year or operating cycle or where liquidation is expected to require the use of existing current assets.

For financial statement reporting, generally the current portion of a long-term liability is reclassified as a current liability and is disclosed in the notes to the financial statements.

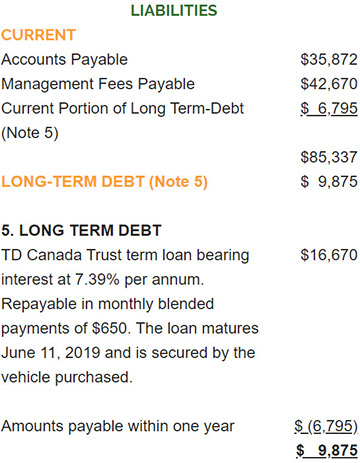

Example – Reclassifying the Current Portion of a Long-Term Debt

Excerpts from a sample balance sheet as at July 31, 2016 and notes to financial statements:

In a computerized accounting system, accounts are identified with the type of account and which is used by the system in categorizing the account, particularly when preparing financial reports, including financial statements. (note: Class is the term used for departments in QuickBooks, so is very confusing if used here)

Assets and Expenses

When a business outlays funds, the first issue to be addressed is whether the outlay represents the purchase of an asset or an expense.

When a business outlays funds, the first issue to be addressed is whether the outlay represents the purchase of an asset or an expense.

If an outlay is expected to yield benefits only in the current accounting period, it would be expensed. Examples of income-account expenditures include office supplies, wages, bank charges and rent paid.

Inventory purchases are like expenses in that they are expected to yield benefits within a short period of time. However, they differ in that an inventory purchase creates an asset whose value will be realized (and expensed) only when the asset is sold. Examples of purchases on inventory account would include books at a bookstore or produce at a grocery store.

Capital expenditures are generally expected to yield benefits beyond the current accounting period. A capital expenditure results in the creation of a capital asset, and the expenditure is capitalized to the balance sheet and amortized over a number of years. Examples of capital assets include computer hardware, machinery and furniture.

For accounting purposes, capital assets are classified as tangible and intangible depending on whether these assets have physical substance (property is tangible if it can be touched or felt). Tangible assets may be referred to as ‘capital assets’, ‘fixed assets’, ‘plant’ or ‘property, plant and equipment’.

There are three general categories of tangible assets: land – held for use in operations but not subject to amortization; buildings, fixtures, equipment – subject to amortization; and natural resources – subject to depletion.

Intangible assets do not have a physical substance but are assets of a business because of the rights they confer on the business. Examples of intangible assets are patents, franchises, copyrights, trademarks, licenses, organizational costs and goodwill. Intangible assets are generally subject to amortization.

A business may create a capital asset for its own use – build a building or a machine, for example, or develop a process which the business patents. All incremental costs associated with the creation of the asset, including materials, labour and related overhead costs (such as utility costs and maintenance on equipment) should be capitalized as part of the capital cost of the asset.

As with liabilities, most computerized accounting systems include asset account categories which are used in classifying and reporting assets.

Time Payments and Prepayments

Occasionally, a vendor may request either a prepayment or a series of prepayments (time payments) from a business prior to the delivery of goods or services. The prepayments or time payments may be made to a vendor by cheque, credit card or cash.

As an outlay of funds, a prepayment is normally processed through the accounts payable/purchasing/cheque issuing system. Such an outlay is, however, an asset of the business as it is not settling a debt but creating a right to the future delivery of property or services from the vendor.

Bank Reconciliation

All businesses have bank accounts and general ledger accounts for each bank account. Because transactions are typically recorded in the books at a time which is not the same as the time the bank records the transaction, it is necessary to reconcile periodically the balance in the general ledger to the balance reported by the bank in the bank statement. This should be completed immediately once the bank statement is received to ensure accurate balances are available.

Most computerized accounting systems include a utility which assists in preparing this reconciliation. Each account will require its own reconciliation. When setting up the reconciliation for the first time in the software, the previous month’s manually prepared reconciliation will be required to enter the required information.

Conclusion

The chart of accounts for a business should reflect the characteristics of that business. Most computerized accounting systems come with pre-established accounts for a variety of business profiles.

All businesses must classify liabilities as either current or long-term. Similarly, outlays must be distinguished between those that create assets and those which should be expensed.

Most computerized accounting systems include asset and liability categories which are associated with general ledger accounts and are used in classifying the accounts for financial reporting purposes.

We can assist you with designing a cohesive Chart of Accounts and navigating the International Financial Reporting Standards for your Small Business in White Rock, Langley or Surrey, BC. Here at Green Quarter Consulting - Accounting and Bookkeeping Services for Small Businesses in White Rock South Surrey, Langley and Surrey BC, we assist Small Business Owners with analyzing transactions, sources of income and your tax risks and how they relate to your business strategy.

Contact us today at 778-791-2864 or 604-970-0658, let’s talk, or send us an email here and we will be in touch very shortly.

GET YOUR FREE CONSULTATION TODAY

![]()

![]()

![]()

![]()

![]()

![]()

Copyright © Green Quarter Consulting, Accountants and Bookkeeping Services White Rock BC 2013–