SALES TAXES IN CANADA - WHAT YOU NEED TO KNOW

GST, PST & HST Canada – The Definitive Guide to Canadian Sales Taxes

Introduction

Sales taxes in Canada are imposed at two levels.

The federal government levies a national sales tax, the GST. Several provinces – British Columbia, Saskatchewan, Manitoba, Quebec and Prince Edward Island – levy a separate retail sales tax often known as PST or combined to create the HST – but what do these mean, and how are they levied, paid or accounted for?

We will review the accounting for these taxes and identify certain industries which are singled out for special sales tax treatment under the GST.

GST

The Goods and Services Tax is the federal national sales tax. It applies to most goods and services.

As noted below, the GST is collected at a different rate when the related sale is made in Newfoundland and Labrador, Nova Scotia, New Brunswick, and Ontario. Tax collected at this rate is commonly referred to as the ‘harmonized sales tax’ or HST. It is important to note, however, that although the rates are different this tax is the same tax as the GST.

Registrant

A registrant is any person—either an individual or business—who is either registered to collect GST or who is required to be registered. So, even though an enterprise might not have registered under the GST system, it will be required to account for tax on the taxable supplies it makes if it is required to be registered.

A registrant is any person—either an individual or business—who is either registered to collect GST or who is required to be registered. So, even though an enterprise might not have registered under the GST system, it will be required to account for tax on the taxable supplies it makes if it is required to be registered.

Everyone who makes a taxable supply in Canada is generally required to be registered. However, a person is not required to be registered – but can elect to do so voluntarily – if that person is a small supplier at the time the supply is made.

It should be noted that a person can never be a small supplier in relation to a taxicab business for HST or PST, so that all taxicab operators are registrants, at least as far as the taxi business is concerned.

The small supplier exclusion also does not apply to the supply of real property by way of sale. Such a supply is always taxable, if it is during a commercial activity.

Commercial Activity

Only a supply made during a commercial activity is subject to tax. The definition of a commercial activity is like, but not identical with, the definition of a business for income tax purposes.

From a practical perspective, most enterprises are engaged in commercial activities unless they are making only exempt supplies, as described below. The default conclusion should always be that the enterprise should be registered and collecting tax in the form of GST, PST or HST as applicable unless it can be shown that it is either a small supplier or is making only exempt supplies.

Taxable Supply

A taxable supply is one made during a commercial activity. Once a supply has been found to be taxable, the question to be addressed is: at what rate?

Effective January 1, 2008 the default rate is 5%, before that date the rate of GST was 6% and prior to July 1, 2006 it was 7%.

Where a supply is zero-rated, the rate is 0%.

Where the supply is made in a harmonizing province which implies HST is to be applied (Nova Scotia, New Brunswick, Newfoundland and Labrador, Prince Edward Island, and Ontario) and the supply is not zero-rated, the rate is 15% (13% in Ontario).

It is almost never necessary to keep track of how much tax is either collected or paid at the 5% rate versus the higher 13, or 15% rate. The tax paid or collected, at whatever rate, is simply aggregated for GST reporting purposes. (An exception is made for certain financial institutions, which are required to track separately the tax paid at 5% and at the higher level)

Zero-Rated Supplies

Zero-rated supplies are those listed in Schedule VI to the Excise Tax Act. The most common categories of zero-rated supplies for GST, HST & PST are basic foods, exports, prescription medicines and most agricultural products.

No tax is collected on a zero-rated supply. However, because a zero-rated supply is a taxable supply, the person making it is required to be registered (unless a small supplier) and can therefore recover tax paid on inputs as an input tax credit. The net result that there is no GST buried in the cost of zero-rated supplies; the consumer acquires them free of any tax.

A taxable supply that is not zero-rated and that is made in a participating province is taxed at a rate of 15% (13% in Ontario).

There are confusingly complex rules which govern how one determines where a supply is made to determine the correct rate of GST, HST or PST applicable. The simplest (and the one used the most) deals with physical goods: it is the place the goods are delivered or made available that governs the rate of tax; not the place where these goods are used.

EXAMPLE – PLACE OF SUPPLY OF GOODS

A business in Alberta sells physical goods (let’s say they are Cordless Tools) to three customers.

The first is in Alberta and the goods are delivered there. This supply takes place outside the participating provinces for HST and so is only subject to GST at 5%.

The second customer is based in New Brunswick and the goods are delivered there. This supply takes place in a participating province so is subject to HST at 15%.

The third customer is also based in New Brunswick but picks up the goods at the business’s warehouse in Grande Prairie. This supply physically takes place in Alberta and is subject to GST at 5%, even though they will be used in New Brunswick.

Exempt Supplies

An exempt supply is defined not to be made in the course of a commercial activity. A person making such a supply does not collect GST on the consideration but is also denied an input tax credit for any tax paid on related inputs. As a result, any GST paid on costs that relate to making exempt supplies is effectively buried in those costs and added into the retail price of the goods for a purchaser.

The major categories of exempt supply are residential rents, sales of used housing, most medical services and most degree programs run by post-secondary colleges, universities, and vocational schools.

Input Tax Credits

The GST is a multi-stage tax, in that it is charged every time goods or services are supplied. For example, a manufacturer might buy raw materials to use in producing goods. Tax would be paid on these materials. When the manufacturer sells the goods to a wholesaler, the manufacturer charges GST to the wholesaler. A mechanism must therefore be provided to allow the manufacturer to recover the GST paid on its inputs, otherwise tax would cascade as the goods or services make their way to the ultimate consumer.

The recovery is called an ‘input tax credit’. A registrant offsets the GST paid or payable in a reporting period against the tax collected or to be collected in that period. If the recovery exceeds the liability, the CRA will refund the amount. If the liability exceeds the recovery, the registrant remits only the net amount.

In order for an input tax credit to be available, GST must be:

- paid or payable by a registrant. A non-registrant cannot recover GST paid as an input tax credit;

- related to the making of a taxable supply. GST paid, even by a registrant, that relates to the making of an exempt supply, cannot be recovered.

It is possible that a GST registrant will make both taxable and exempt supplies, although such enterprises are rare. A business that makes both types of supplies must allocate the GST it pays between that which relates to commercial activities and which can be recovered as an input tax credit and that which relates to making exempt supplies, which cannot be recovered.

Where GST must be allocated, there are fairly complex rules which determine how the allocation is to be made. These rules vary with the type of expenditure.

Input Tax Credit Restrictions

All enterprises, including those that make only taxable supplies and which are engaged exclusively in commercial activities, face restrictions on the recovery of GST on certain types of expenditures. These include 50% of the tax paid on meals and entertainment expenses which are limited for income tax purposes; tax paid on expensive passenger vehicles; tax paid on club memberships; and tax paid on expenditures which are not deductible for income tax purposes because they are personal to the owner of the business.

Rebates

In addition to claiming an input tax credit, certain enterprises are allowed to recover tax that cannot be claimed as an input tax credit as a rebate.

Where a rebate is available, the tax to be recovered is not related to commercial activities but must be tracked separately for recovery.

For example, a hospital authority is allowed to recover as a rebate 83% of the GST it pays which cannot be claimed as an input tax credit. The hospital would therefore need to keep a separate general ledger account in which it tracks GST paid which cannot be recovered as an input tax credit. Most public sector bodies, which make largely only exempt supplies, recover some of the GST they pay as a pro-rata rebate.

Bookkeeping GST

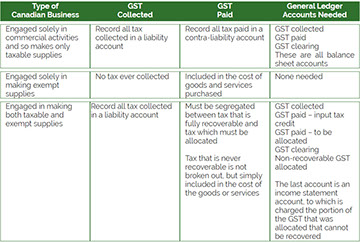

The way in which GST is accounted for and the accounts to be set up in the general ledger to account for it depend on the nature of the enterprise but can be summarized in the table which follows. It should be noted that some computerized accounting systems have built in Sales Tax components, and therefore only one account is required.

The way in which GST is accounted for and the accounts to be set up in the general ledger to account for it depend on the nature of the enterprise but can be summarized in the table which follows. It should be noted that some computerized accounting systems have built in Sales Tax components, and therefore only one account is required.

In the vast majority of cases, a GST registrant business enterprise will be engaged solely in commercial activities. For these, the major accounting challenge is to ensure that GST/HST is charged at the correct rate on all revenues and that all tax paid is captured for recovery as an input tax credit.

The GST related to the transactions for such an enterprise appear on the balance sheet and GST does not flow through the income statement. Where such an enterprise is subject to the general input tax credit restrictions described above, the portion of the tax that is not recoverable is included in the cost of the related expenditure and is not recorded separately and therefore does flow through the income statement.

The next most commonly encountered Canadian Company scenario is the business that makes only exempt supplies – such as a medical doctor, a dentist or an insurance brokerage. For these the accounting is even simpler, as no tax is ever collected and all tax paid is not recoverable and need not, therefore, be segregated.

Rarely, a Canadian Company will make both taxable and exempt supplies. For these, tax paid must be allocated. That which relates to making taxable supplies is fully recoverable. That which relates to making exempt supplies is not recoverable and is included in the related cost. That which relates to both types of supplies must be segregated and allocated separately.

There are no fixed rules on how tax is to be allocated in these circumstances. Any reasonable method can be used, so long as it is applied consistently in the year.

The GST clearing account is used at the end of each reporting period to zero out the accounts for tax collected and input tax credits for the applicable Canadian Company. Using a clearing account creates clear trail from the two tax accumulation accounts to the net amount that appeared on the GST return.

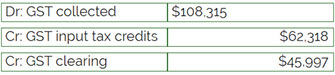

EXAMPLE – GST CLEARING

ABC Inc. a Canadian Company, reports GST monthly. At the end of January 201X, ABC’s GST collected liability account shows a credit balance of $108,315, representing the GST on sales for the month. The GST input tax credit account shows a debit balance of $62,318, representing the GST paid in the month.

ABC Inc. posts the following entry at month end:

The $45,997 net liability is the amount that appears on the GST return for the period and which is itself cleared by the cheque that ABC Inc. cuts when it remits the net tax.

Reporting GST for a Canadian Company

Every Canadian GST registrant is required to file a GST return based on the registrant’s reporting period. Most Canadian Companies file quarterly; large enterprises file monthly; smaller enterprises file annually and pay quarterly installments. An enterprise can always elect to file more frequently than its regular reporting period, and an election to file monthly, for example, is typically beneficial where the enterprise is usually in a refund position. This would be true for a business that has largely zero-rated revenues, such as one that exports most of its sales or that sells agricultural products.

Every Canadian GST registrant is required to file a GST return based on the registrant’s reporting period. Most Canadian Companies file quarterly; large enterprises file monthly; smaller enterprises file annually and pay quarterly installments. An enterprise can always elect to file more frequently than its regular reporting period, and an election to file monthly, for example, is typically beneficial where the enterprise is usually in a refund position. This would be true for a business that has largely zero-rated revenues, such as one that exports most of its sales or that sells agricultural products.

On the GST return, the enterprise reports GST collected and GST recoverable as an input tax credit. Certain other adjustments (such as the recovery of GST included in a bad debt written off) are also reported. The net amount, called ‘net tax’, is calculated. If it is a negative number, it is refunded by CRA. If it is a positive number, the enterprise pays the amount with its return.

A new Canadian business anticipating sales necessitating GST, or a business that was previously not registered but is now required to register or chooses optionally to register, is required to obtain a GST registration number. The number is simply the business number that the business has (or obtains, if it is a new business), to which a GST account is appended.

Registration is a fairly simple process, and can be accomplished in person, by phone, by mail, by fax or on-line. In Quebec, the Quebec Ministry of Revenue administers both the Quebec retail sales tax (QST) and the GST and Quebec businesses register with the Ministry for both taxes.

Simplified Accounting Methods

Certain smaller enterprises are allowed to compute and report net tax using a so-called ‘simplified’ accounting method. The simplified methods are based on the business not breaking out the GST collected or paid, but calculating a net tax amount by applying a percentage to their GST-included revenues.

Where an enterprise qualifies to use one of the simplified accounting methods, there is no need to break out either tax collected or tax paid. Rather, it is the tax-included revenue that will determine the amount of tax to remit.

The Quick Method of Tax Accounting for GST, HST, QST & PST

The Quick Method can be used by any Canadian business whose taxable supplies for a year do not exceed $400,000 (beginning in 2013), including that of associated businesses (remember that zero-rated supplies are taxable supplies and must therefore be included). Revenue from the sale of capital property and provincial retail sales taxes collected are excluded from the $400,000 base. The Quick Method cannot be used by a business providing legal, accounting or consulting services.

Where a business chooses to use the Quick Method, it calculates the net tax to remit by applying a prescribed rate to its GST-included revenues. Such an enterprise cannot generally claim input tax credits, except that credits are still permitted for the GST paid on capital expenditures.

Simplified Method for Input Tax Credits in relation to GST, HST, QST & PST

A Canadian Company with annual taxable revenue, including that of associated businesses, of less than $1,000,000 in its preceding year and annual GST taxable purchases of less than $4,000,000 can elect to use a simplified method for claiming input tax credits. The input tax credits are calculated as 5/105ths or 15/115ths of the tax-included cost of the purchases (13/113 in Ontario).

This option is available to small businesses, charities, not-for-profit organizations, and selected public service bodies.

An enterprise that chooses to use this method need not break out the GST paid on inputs.

Special Cases of Canadian Companies for Taxes

Certain types of activity are singled out for special GST treatment.

AGENTS AND AUCTIONEERS

Special rules are provided to simplify the accounting for GST where property of one person is sold by another – an agent in general or an auctioneer. While these rules are complex, they are intended to make life easier and will often be used when it would be too difficult to have the principal account for the GST.

DIRECT SELLERS

Direct sellers are independent sales agents (such as Amway distributors, or Avon representatives) who solicit orders for the delivery of inventory by a third party.

Simplifying rules are also available for this sector, which push the GST accounting back from the direct seller to the company which the seller represents.

RETAIL (PROVINCIAL) SALES TAX (PST) AND QUEBEC SALES TAX (QST)

Unlike the GST, which applies to all transactions but is refunded to those engaged in commercial activities, retail sales taxes are generally applied only to the final consumer. (A major exception, however, is QST. Although it is a provincial sales tax, it works in much the same way as GST and is refunded to registrants who make taxable supplies, so that it is generally levied only on the final consumer.)

Where an intermediary purchases goods or services that are subject to PST, but which have been acquired for resale, the purchaser provides an exemption number to the vendor and is relieved from paying tax. It is only the final sale to the consumer that attracts tax.

Where goods have been purchased for resale with PST and are subsequently diverted for use by the business, the business is required to self-assess PST if the goods are used in a PST province. Self-assessment is based on the fair value of the goods, not their cost.

EXAMPLE – PAYING PST FOR CANADIAN COMPANIES

Acme Inc. is a retailer of office supplies. It buys computer printer cartridges which it intends to resell. Acme quotes its PST registration number to the wholesaler of the cartridges. This number allows the wholesaler to sell the cartridges to Acme without charging PST. Acme, of course, charges PST when it sells a cartridge to a consumer.

Sometime later, Acme removes 10 cartridges from inventory and installs them in its own printers. The retail value of the cartridges is $200.00, their cost is $150.00 and the provincial PST rate is 7%

Acme must record the transfer of inventory and the liability for tax:

It will be clear that PST paid is only rarely recoverable and as a consequence is generally included in the cost of the goods or services purchased.

PST collected, on the other hand, must be remitted.

PST Base

There is some variation between the provinces in what is subject to PST. Initially, PST was applied only to goods. With time, however, many provinces have expanded their PST bases to tax services as well, although the services that are subject to tax vary by province.

In Quebec, the Quebec Sales Tax is levied on a tax base that coincides pretty well with the GST base, so that QST is charged on most goods and services.

In provinces where PST is applied such as British Columbia, Manitoba and Saskatchewan, the PST is charged on the same amount that attracts GST. In Quebec, the provincial sales tax is charged on the GST-included amount.

Registering for and Collecting Tax

The various provincial regimes generally require that any person who makes a retail sale into a province is required to register and collect the province’s tax. As a practical matter, most enterprises that do not have a fixed place of business in a province ignore this requirement and only collect PST on sales made in those provinces where the business has offices. Where tax is not collected on a retail sale into a province, it is the purchaser who is supposed to self-assess the related tax.

KEY CONCEPTS for CANADIAN COMPANY SALES TAXES

- Sales taxes are levied by both the federal and certain provincial governments, typically on different sales bases.

- GST and HST are the federal taxes. For most Canadian businesses these taxes are fully refundable.

- GST reporting will generally require three balance sheet accounts: GST paid, GST collected, and GST clearing.

- Businesses such as exporters will generally be in a GST/HST refund position since exports are zero-rated. These businesses will likely want to file monthly returns to improve cash flow.

- PST is levied by certain provinces. For most businesses, PST paid is not recoverable. Where goods (and limited services) are purchased for resale, the business can typically buy them without paying PST by quoting its PST registration number.

- Many businesses choose not to register for PST in provinces where they don't have a place of business, but provincial laws require such registration.

- The bookkeeping system for Canadian Companies should be set up to track those taxes that must be remitted – GST/HST/QST and PST collected, and those taxes that can be recovered – typically only GST/HST/QST.

We can assist you with determining how to account for Federal and Provincial Sales Tax in Canada for your Small Business in White Rock, Langley or Surrey, BC. Here at Green Quarter Consulting - Accounting and Bookkeeping Services for Small Businesses in White Rock South Surrey, Langley and Surrey BC, we assist Small Business Owners with analyzing transactions, sources of income and your tax risks and how they relate to your business strategy. Learn more about our Greenstamp CFO Services here.

We can assist you with determining how to account for Federal and Provincial Sales Tax in Canada for your Small Business in White Rock, Langley or Surrey, BC. Here at Green Quarter Consulting - Accounting and Bookkeeping Services for Small Businesses in White Rock South Surrey, Langley and Surrey BC, we assist Small Business Owners with analyzing transactions, sources of income and your tax risks and how they relate to your business strategy. Learn more about our Greenstamp CFO Services here.

Contact us today at 778-791-2864 or 604-970-0658, let’s talk, or send us an email here and we will be in touch very shortly.

GET YOUR FREE CONSULTATION TODAY

![]()

![]()

![]()

![]()

![]()

![]()

Copyright © Green Quarter Consulting, Accountants and Bookkeeping Services White Rock BC 2013–